|

|

|

|

|

|

| Appointing four financial advisers shows CIMC and SDIC's determination to close the privatisation deal |

HONG KONG, Dec 3, 2020 - (ACN Newswire) - On 30 November, CIMC-TianDa issued a joint announcement regarding, among other matters, the dispatch of privatisation scheme circular.

According to the announcement, Sharp Vision, a wholly-owned subsidiary of CIMC, and Expedition Holding, as the joint offerors, made a privatisation proposal to CIMC-TianDa. The privatisation price is HK$0.266 per share, a 20.36% premium to the closing price of HK$0.221 on the last trading day.

Assuming that Sharp Vision will not exercise the right to convert its convertible bonds, the joint offerors and their concert parties hold 12.574 billion shares, representing approximately 75.58% of the issued share capital of CIMC-TianDa, while independent shareholders hold 4.064 billion shares, representing approximately 24.42% of the issued share capital. The maximum amount of cash consideration required to effect the privatisation proposal will be HK$1.082 billion.

As shown in the announcement, the joint offerors and their concert parties have appointed ABCI Capital, Zhongtai Capital and Donvex Capital as their joint financial advisers (FA) in connection with the privatisation proposal. In its announcement issued on 19 October, CIMC-TianDa has appointed Gram Capital Limited as the independent financial adviser to advise the Independent Board Committee.

The fact that a total of four financial companies provide professional advice in a privatisation case of this magnitude is groundbreaking, which reflects the determination of the joint offerors and their concert parties for a successful privatisation scheme.

As shown in the shareholding structure, Sharp Vision is a wholly-owned subsidiary of CIMC, while Expedition Holding is wholly-owned by Macao QiXin Investment Management Limited whose shareholders are CNIC of SDIC, TUS-S&T Service Group, and Tus-Financial Group. These three SOEs are strong shareholders with extensive experience and professional talents in the fields of international investment and M&A, national strategic investment, private equity investment in emerging industries, start-up investment, asset management, and financial investment banking services. The combination of QiXin Investment and the four competent financial advisers demonstrates the resolution of CIMC and SDIC in succeeding the privatisation deal.

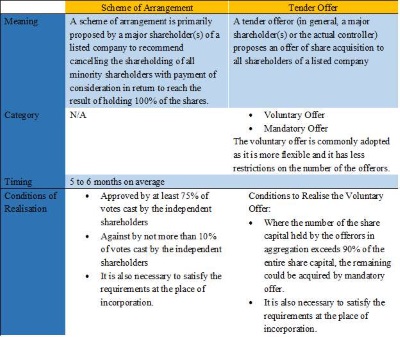

CIMC-TianDa plans to be privatised by way of a scheme of arrangement, a higher probability of success

There are two main ways to privatise a listed company in Hong Kong - one is by way of a scheme of arrangement and the other is by way of a voluntary general offer.

These two privatisation ways share one thing in common, which is that the controlling shareholders, as the joint offerors, and their concert parties, don't get to vote, even if they hold a majority of shares. In fact the success of a privatisation proposal depends on the votes of independent shareholders.

The difference is that, in the case of privatisation by way of a voluntary general vote, it requires not only the approval of independent shareholders through voting at the extraordinary general meeting (EGM), but also that independent shareholders should, on the basis of their shareholdings, accept the offer made by the offerors. When the offer period ends, the offerors will have to obtain acceptances which in aggregate represent no less than 90% in value of the shares for which the offer is made.

It is quite a demanding requirement to satisfy. Some shareholders may find the offer price unattractive, while others may not even notice the offer information. As a result, the threshold for privatisation by way of a voluntary offer is very high, which is generally less appealing to independent shareholders.

Relatively speaking, privatisation by way of a scheme of arrangement in Hong Kong stock market stands a higher probability of success.

Based on public information on the HKEX website, from January 2019 to September 2020, 33 privatisation offers had been announced by companies listed on the HK's stock exchange (excluding those made by H-share companies). Among which, all the 11 privatisation proposals announced in 2019 were completed with shares delisted. For the 22 offers announced during the nine months ended 30 September 2020, one offer closed without being privatised, seven were successfully completed, one is pending listing withdrawal, and 13 are ongoing. Out of the 33 privatisation offers, only three were made through voluntary general offers, while the remaining 30 were made by way of schemes of arrangement.

Moreover, based on the SOE privatisation cases, it can be concluded that privatisation by way of a scheme of arrangement is more likely to succeed. We'd like to elaborate on it with two typical examples, a successful one and a failing one. On 27 September 2018, Sinotrans Shipping (0368.HK) made an announcement, proposing the withdrawal of its listing and privatisation by way of a scheme of arrangement. At the EGM held on 13 December 2018, 99.3% of the shares held by independent shareholders were voted in favour of privatisation, and only 0.7% of the shares were voted against it. At the Court Meeting held on the same day, 95.8% of the votes held by independent shareholders voted in favour of privatisation, while only 2.0% voted against it. As the conditions were fulfilled, the listing of Sinotrans Shipping on the Hong Kong Stock Exchange was withdrawn on 16 January 2019 and the privatisation was completed.

Another SOE privatisation proposal is that on 12 December 2018, Harbin Electric Company (1133.HK) and its parent company, Harbin Electric Corporation, made a joint announcement that Harbin Electric Corporation would make a voluntary conditional cash offer to acquire all the issued H Shares of Harbin Electric Company (i.e. by way of a voluntary general offer). The H Share Offer was HK$4.56 in cash for each H Share. In the following process, although the deal was approved at the general meeting of shareholders, the offer failed to meet the 90% threshold for acceptance of independent shares within the prescribed period, thus declaring the privatisation unsuccessful. The company's share price plunged from around HK$3.80 all the way to the lowest HK$1.45, with a cumulative decline of over 60%.

The latest quotation of Harbin Electric, which is still listed, is HK$2.52 per share, lower than the privatisation offer price proposed by the offeror two years ago. The market risks associated with a failed privatisation offer can be extremely significant. Unless the assets of the target company are of particularly high quality, or unless the majority shareholders and their concert parties believe that the timing is right, the chances of going private again are actually slim.

State-owned enterprise privatisation adopts the more successful, more reliable and much easier approach. Actually, it should also exemplify the deep sense of responsibility of any offeror to safeguard the interests of all shareholders.

However, we could return to the analysis of the privatisation case of CIMC-TianDa. the Company chose the scheme of arrangement for its privatisation proposal in accordance with its circular.

For the priviatisation under a scheme of arrangement, two conditions as below shall be firstly fulfilled:

(1) at the Court Meeting of privatisation, the scheme shall be approved by more than 75% of the votes cast by the independent shareholders present at the meeting;

(2) at the Court Meeting of privatisation, the scheme shall not be against by more than 10% of the votes cast by the independent shareholders present at the meeting.

In addition, we are required to pay attention to the matters in relation to the place of incorporation as it is necessary to satisfy relevant requirements stipulated by that place apart from the above two conditions to undertake the privatisation by the way of a scheme of arrangement. Many investors are often hindered by blind spots due to lack of professional expertise, ultimately influencing their investment decisions and judgments, which is common for the privatisation at Hong Kong share market.

We would take the privatisation of CIMC-TianDa as an example. The circular indicates that the Company is a listed company incorporated in Cayman Islands. In accordance with Section 86 of Companies Law of the Cayman Islands, a listed company in Cayman Islands has to fulfil the requirement for proposed privatisation: more than 50% of the shareholders present at the Court Meeting approve the privatisation proposal, no matter the number of the shareholding held by such shareholders, commonly referenced to as Clause of "Head Counting".

Under this situation, where the privatisation proposal is approved by voting at the general meeting and the court meeting and other conditions for privatisation have been fulfilled (Clause of "Head Counting"), the independent shareholders could just await until the listed company takes over their shares in accordance with the remaining procedures and returns them the considerations. In conclusion, once the conditions of the privatisation have been fulfilled, the shareholding of independent shareholders shall be taken away ultimately. No matter whether these independent shareholders have participated in the voting or voted against the proposal, they shall comply with the final resolution passed by the general meeting and the court meeting on the basis of the "Majority Rule".

Where the companies incorporated in PRC are desirous to undertake privatisation by means of a scheme of arrangement, they don't have to abide by the Clause of "Head Counting". Meanwhile, in accordance with the Company Law of the People's Republic of China, the shares of the medium and small shareholders shall not be taken over by mandatory offer. Regarding the listed companies registered in mainland China, the independent shareholders are protected to proactively submit their application of acceptance for their shares in accordance with relevant offer and transfer their shares to an offeror even the privatisation is approved by votes at the general meeting. Otherwise, the independent shareholders who have not accepted the offer will become the shareholders holding the non-negotiable shares after their listed company delists in accordance with the privatisation procedures.

Identifying the arbitrage opportunities behind the privatisation, the "winner-takes-all" will elevate the success rate of privatisation

With the above discussions, we could observe that the listed companies registered in Cayman Islands have the strength to approach privatisation more easily and they are privatised more completely if they succeed in privatisation. Moreover, it is important that it is easier for them to achieve cohesion and win-win situation with independent shareholders and avoid the chance of intense wrangling and severe confrontation.

Coming back to the perspective of market and transactions, it is more likely to produce the fixed mode of arbitrage as it is more predictable. In other words, it is more likely to attract leading investment companies or individual and investment organisations to increase the share capital to facilitate the approval of relevant proposal and realise the expected return of the consideration in the offer of privatisation in short term.

With conclusion and summarisation of numerous privatisation cases, we found that as long as the privatisation proposal is implemented by means of a scheme of arrangement(instead of the voluntary general offer), companies are the listed companies registered in Cayman Islands(required to comply with Section 86 of the Companies Laws of Cayman Islands) and the dominant controlling shareholders and their persons acting in concert work together to expedite and implement such project, the implied essence is "winner-takes-all" under the principle of the privatisation.

Now we could consider and reason from the perspective of a qualified leading investment company or individual or a professional organisation and approach to understand purely in terms of expected rate of return or expected annualised rate of return and assets allocation.

As the circular demonstrates, the court meeting and the EGM shall be convened within this month. If it is approved successfully, the shareholding of each independent shareholders shall be delisted on the stock exchange with the procedures on 25 January of next year and effect on the same day as expected. The independent shareholders are expected to receive the cash cheque paid by the offerors and their concert parties of the privatisation on or before 1 February of next year.

At the court meeting and the EGM, if the privatisation proposal is passed, alternatively, after the "Showdown", the subsequent procedures shall be followed as routine and the uncertainties will be eliminated. On that basis, the share price of CIMC-TianDa is likely to soar close to HKD 0.2666 per share after the proposal is passed and it is the period to realise fastest growth of the rate of return.

So now let's do some calculations. Based on the closing price of CIMC-TianDa at HK$0.245 on 1 December, the privatisation implied an absolute return of 8.57% after the resolution was passed. We will roughly take 8% as the expected rate of return for the calculation. From 2 December to 28 December (the first trading day when the voting result is announced), there are only 27 calendar days. The expected annualised rate of return appropriately exceeds 100%., It is impossible not to attract their attention from large capital allocation perspective.

If they do, the biggest risk they face is actually the rejection of the privatisation proposal. Then just work hard in the direction to get the privatisation proposal passed. What should we do? It's very simple. There are only three action points: (1) Observe market trends and seek for conspirators; (2) Buy the shares, attend the general meetings and court meetings as independent shareholders, and vote in favor of the privatisation proposal; (3) Reasonable assumptions and verification, analysis shows that investors who buy into the first two ideas are mostly shareholders.

In fact, the most critical point is the third point, we might as well have a logical deduction.

If independent shareholders expect that the privatisation proposal will not be passed (or the probability of passing is low), the most favorable option for them (in order to avoid risks) is to sell at the current price, rather than to hold onto the shares and wait until the general meeting and the Court Meeting to cast an objection. Because based on rationality and human nature, they most likely will not harm themselves. Therefore, those who will not sell but will vote at the shareholders meeting can be regarded as a negligible small group.

The second type refers to those who hold onto the shares but will no vote at the shareholders meeting, which we can ignore as they will not affect the polling result.

The third type refers to those who have sold the shares. Since shares have been sold, the person loses the voting right and has no impact on the result.

The last type refers to the major crowd, who are holding onto or are continuous buying, and are joining the shareholders meetings to cast the votes. Given their motives and reasons are very sufficient and necessary, which have been discussed above, we will skip the explanation here.

To come to a direct and simple conclusion: opponents will tend to sell; investors who are in favor of the privatisation proposal and can obtain their expected returns on the basis of approval, or form a sound arbitrage model, will prefer hold onto or to continuous buy the shares.

This is driven by the underlying rule of "winner takes all". Under this rule, the probability of the privatisation proposal being passed has been repeatedly blessed and consolidated on the basis of the relatively high probability.

After the announcement of the privatisation proposal of CIMC-TianDa on 4 October, its trading volume continued to be dynamic, as opposed to its previous silent status and the stock price was stable. From a trading perspective, once an investor is willing to sell, then there are always investors on the other side willing to buy. Because the selling power is always lower than the buying power for position accumulation within a certain price range, this causes the stock price to trade sideways. The relatively larger trading volume than the previous period indicates the continuous trading momentum.

Understanding the logic and motives behind the trading and knowing the "calculations" of the core traders in the market is the best answer and explanation for understanding this phenomenon.

We believe, even ordinary investors who will not participate in the voting, should consider the free-rider strategy - a bold attempt to ride on the privatization of CIMC-TianDa for some profits.

Topic: Press release summary

Source: CIMC-TianDa Holdings Company Limited

Sectors: Daily Finance, Daily News

https://www.acnnewswire.com

From the Asia Corporate News Network

Copyright © 2024 ACN Newswire. All rights reserved. A division of Asia Corporate News Network.

|

|

|

|

|

|

|

|